商品期货价格数据的降噪处理:以傅立叶变换和卡尔曼滤波变换为例

0

256

0

256

1. 价格数据降噪处理的重要性

在金融市场中,商品期货的价格往往受到市场波动、噪声以及异常波动的影响。这些噪声可能源于市场的随机性、交易者行为、流动性不足等因素。降噪处理的目的是通过去除价格数据中的短期波动和随机噪声,揭示出价格的长期趋势,从而为投资决策提供更清晰的信号。

降噪处理的意义主要体现在: - 提高分析的准确性:通过消除价格中的随机波动,投资者能够更加准确地分析市场趋势。 - 减少决策风险:降噪后数据的稳定性提高,有助于投资者减少因噪声引发的错误交易决策。 - 提供稳定的技术指标:许多技术分析指标依赖于平滑处理后的数据,降噪处理能够提高这些指标的有效性。

2. 常见的降噪处理方法

在金融数据处理中,常用的降噪方法可分为常规和复杂处理两类:

常规方法:

- 移动均线(SMA):最简单且常见的降噪方法,通过取一定窗口内的数据均值来平滑波动,适合短期趋势分析,但滞后性强。

复杂方法:

- 傅立叶变换(Fourier Transform):通过将时间序列转换为频域信号,并去除高频噪声,从而达到降噪目的。适合处理周期性信号。

- 卡尔曼滤波(Kalman Filter):动态优化每个时间点的估计值,通过引入过程方差和测量方差,能适应数据中的非线性变化,适合实时动态数据的降噪。

- 热方程处理:通过对数据的扩散效应模拟实现平滑效果,较为复杂,适合对多维数据进行处理。

在接下来的部分中,将展示三种典型的降噪方法,包括移动均线、傅立叶变换和卡尔曼滤波,并对其优缺点进行比较。

3. 三种降噪方法的展示

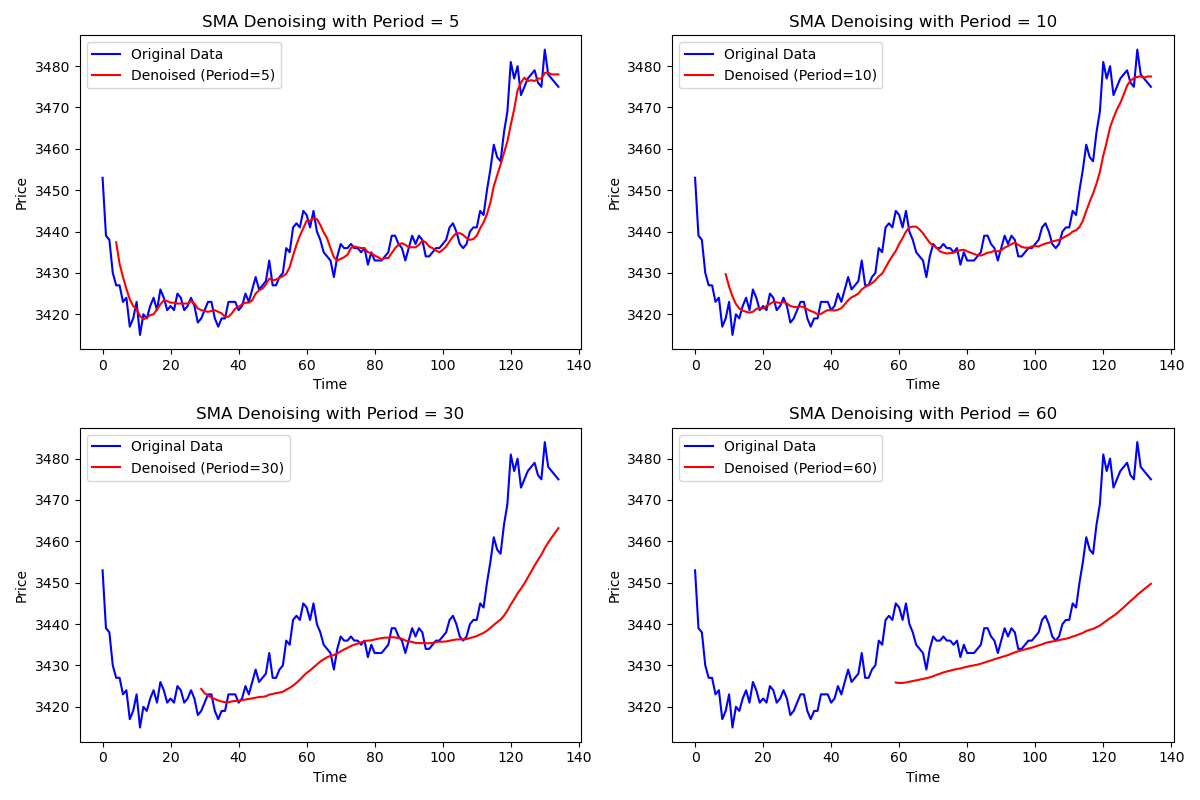

(1)移动均线(SMA)

移动均线通过计算固定周期内的平均值,来平滑原始价格数据,减小短期波动的影响。它的优点是简单易用,但缺点是会引入滞后性,导致对市场变化的响应较慢。

'''backtest

start: 2024-10-10 00:00:00

end: 2024-10-10 09:15:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

args: [["ffthre",0.1]]

'''

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

# 移动均线函数

def calSMA(time_series, period):

moveingAve = TA.MA(time_series, period)

return moveingAve

def main():

while True:

r = exchange.GetRecords('rb2501')

data = pd.DataFrame(r)

time_series = data['Close'].values

data['Time'] = range(len(data))

# 设置不同的周期

periods = [5, 10, 30, 60]

plt.figure(figsize=(12, 8))

# 对不同周期进行降噪并可视化

for i, period in enumerate(periods):

sma_time_series = calSMA(time_series, periods[i])

plt.subplot(2, 2, i + 1)

plt.plot(data['Time'], time_series, label='Original Data', color='blue')

plt.plot(data['Time'], sma_time_series, label=f'Denoised (Period={period})', color='red')

plt.xlabel('Time')

plt.ylabel('Price')

plt.title(f'SMA Denoising with Period = {period}')

plt.legend()

plt.tight_layout()

plt.show()

LogStatus(plt)

Sleep(1000 * 10)

原理说明:移动均线对每个时间点的值取前N个点的平均,平滑短期波动,但引入滞后。

滞后性分析:随着周期的增加,滞后性也会增加,导致趋势信号的延迟。

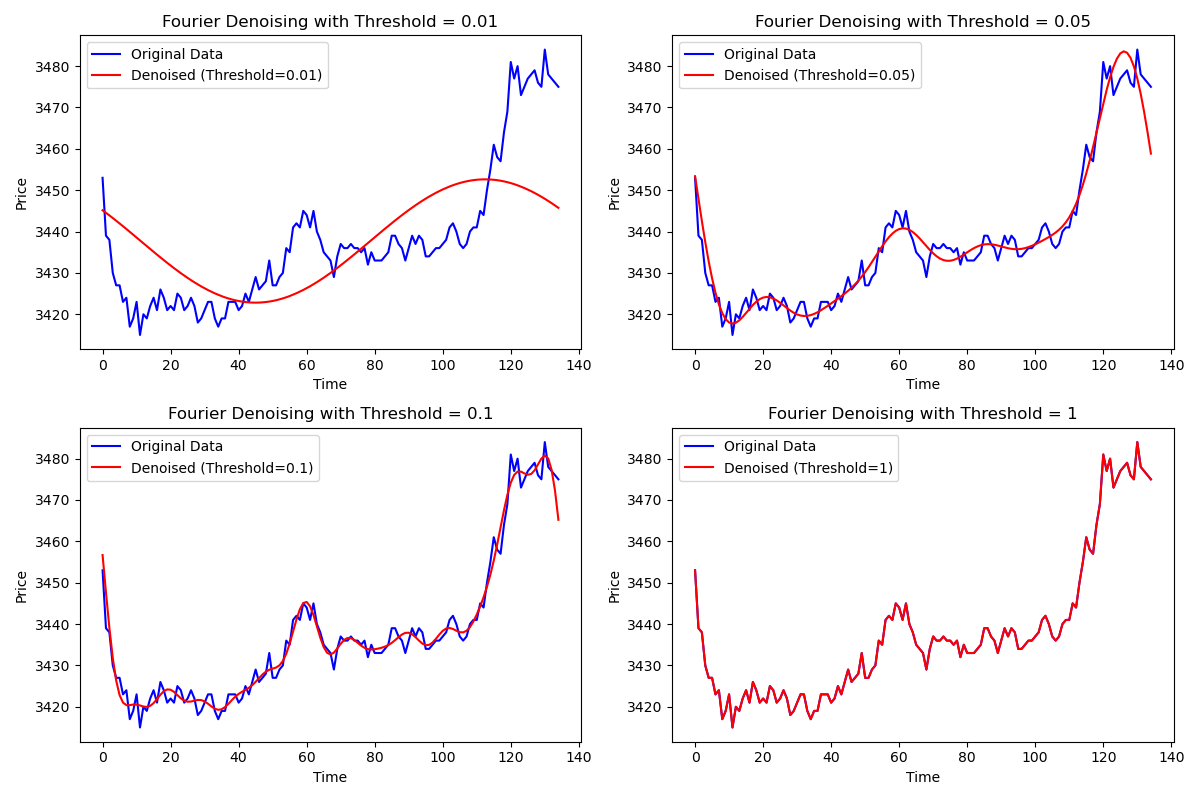

(2)傅立叶变换(FFT)

傅立叶变换将价格数据从时域转换到频域,以便识别其中的周期性成分。通过设置频率阈值,可以过滤掉高频噪声,仅保留低频的趋势信息。

'''backtest

start: 2024-10-10 00:00:00

end: 2024-10-10 09:15:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

args: [["ffthre",0.1]]

'''

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.fftpack import fft, ifft

def fftransform(time_series, ffthreshold):

# 进行傅里叶变换

fft_values = fft(time_series)

frequencies = np.fft.fftfreq(len(time_series))

# 复制傅里叶变换值,进行降噪处理

filtered_fft_values = np.copy(fft_values)

# 根据阈值设置保留的频率范围,超过阈值的频率被设为 0

filtered_fft_values[np.abs(frequencies) > ffthreshold] = 0

# 进行逆傅里叶变换并提取实部(去掉复数部分)

filtered_time_series = ifft(filtered_fft_values)

filtered_time_series = np.real(filtered_time_series)

return filtered_time_series

def main():

while True:

r = exchange.GetRecords('rb2501')

data = pd.DataFrame(r)

time_series = data['Close'].values

data['Time'] = range(len(data))

# 设置不同的阈值

thresholds = [0.01, 0.05, 0.1, 1]

plt.figure(figsize=(12, 8))

# 对不同阈值进行降噪并可视化

for i, threshold in enumerate(thresholds):

filtered_time_series = fftransform(time_series, thresholds[i])

plt.subplot(2, 2, i + 1)

plt.plot(data['Time'], time_series, label='Original Data', color='blue')

plt.plot(data['Time'], filtered_time_series, label=f'Denoised (Threshold={threshold})', color='red')

plt.xlabel('Time')

plt.ylabel('Price')

plt.title(f'Fourier Denoising with Threshold = {threshold}')

plt.legend()

plt.tight_layout()

plt.show()

LogStatus(plt)

Sleep(1000 * 10)

原理说明:傅立叶变换通过频域分析可以有效地分离噪声和趋势。较高的频率对应着噪声,较低的频率对应着长期趋势。傅立叶变换将数据从时间域转换到频域,保留低频信息,去除高频噪声,通过逆变换恢复平滑的时间序列。对周期性信号效果良好。而:对于非周期性信号,处理效果有限。

参数解释:阈值越低,保留的频率成分越多,数据的波动细节更多,降噪效果较弱。阈值越高,保留的频率成分越少,数据变得更加平滑,降噪效果更显著。

图像解释:从图中可以看出,随着阈值的增加,平滑程度增强,降噪效果更为显著。低阈值保留了更多细节,高阈值则更好地滤除了噪声。

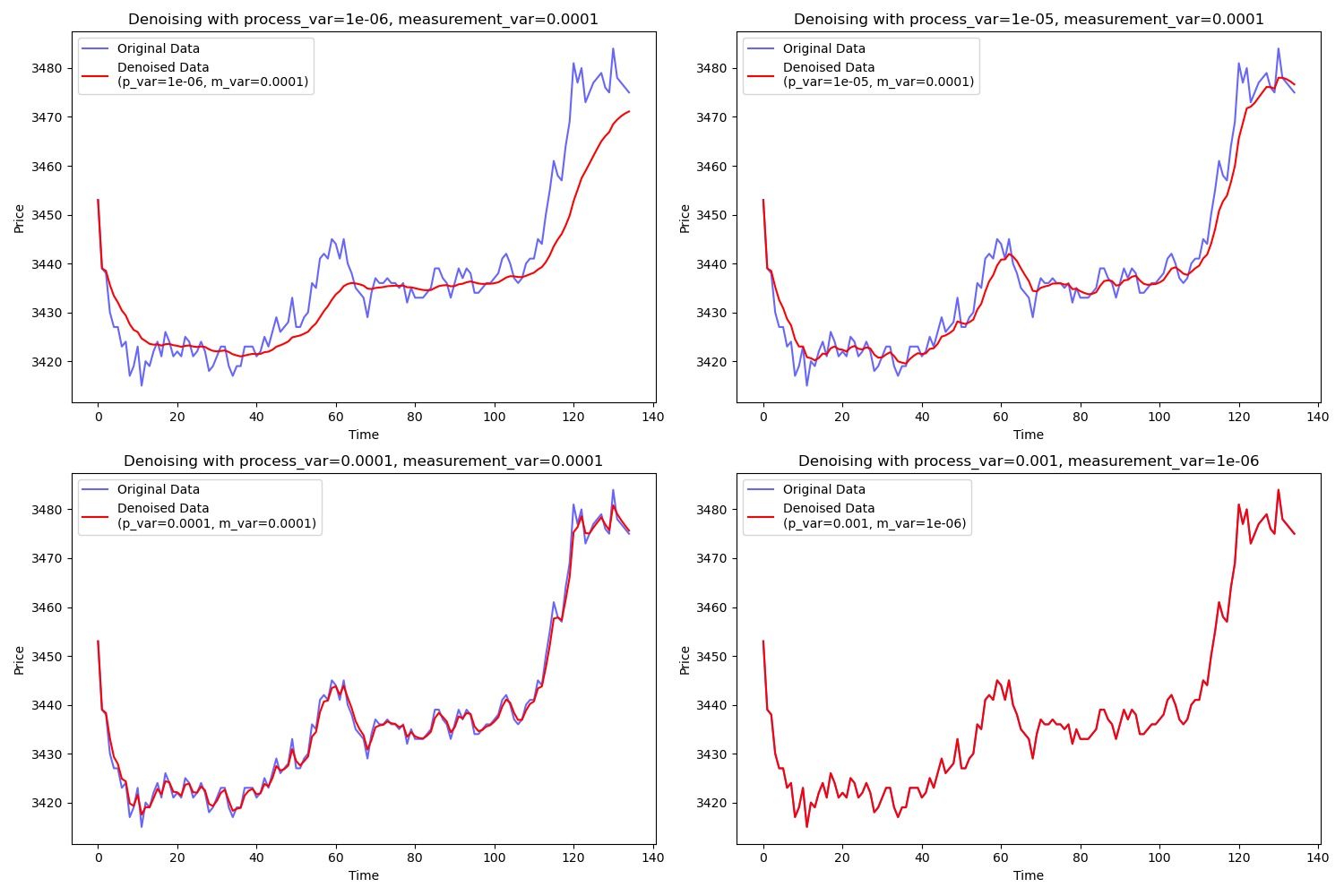

(3)卡尔曼滤波(Kalman Filter)

卡尔曼滤波是一种自适应的降噪方法,能够通过动态调整状态估计来跟踪数据的真实趋势。

'''backtest

start: 2024-10-10 00:00:00

end: 2024-10-10 09:15:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

args: [["ffthre",0.1]]

'''

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

# Kalman 滤波器函数,带有可调的过程方差和测量方差参数

def kalman_filter(data, process_variance=1e-5, measurement_variance=0.01**2):

"""

使用指定的过程方差和测量方差对输入数据进行 Kalman 滤波处理。

:param data: 需要降噪的一维数据(如收盘价数组)。

:param process_variance: 过程方差(默认值=1e-5)。

:param measurement_variance: 测量方差(默认值=0.01^2)。

:return: 使用 Kalman 滤波器处理后的降噪数据。

"""

n = len(data)

# 初始化状态和协方差

estimated_state = np.zeros(n) # 存储每个时刻的状态估计

estimated_error_covariance = np.zeros(n) # 存储每个时刻的估计误差协方差

# 对初始状态和初始协方差进行猜测

estimated_state[0] = data[0] # 初始状态估计设为第一个数据点

estimated_error_covariance[0] = 1.0 # 初始估计误差设为 1.0

# 遍历每个数据点

for i in range(1, n):

# 预测步骤

predicted_state = estimated_state[i-1] # 预测的下一个状态等于前一个估计状态

predicted_error_covariance = estimated_error_covariance[i-1] + process_variance # 预测的误差协方差

# 更新步骤

kalman_gain = predicted_error_covariance / (predicted_error_covariance + measurement_variance) # 计算卡尔曼增益

estimated_state[i] = predicted_state + kalman_gain * (data[i] - predicted_state) # 更新状态估计

estimated_error_covariance[i] = (1 - kalman_gain) * predicted_error_covariance # 更新误差协方差

return estimated_state # 返回降噪后的状态估计值

def main():

while True:

r = exchange.GetRecords('rb2501')

data = pd.DataFrame(r)

time_series = data['Close'].values # 取出收盘价数据

data['Time'] = range(len(data)) # 为时间轴创建索引

# 不同的过程方差和测量方差组合

variance_settings = [

(1e-6, 0.01**2),

(1e-5, 0.01**2),

(1e-4, 0.01**2),

(1e-3, 0.001**2),

]

# 可视化原始数据和不同方差下的降噪数据

plt.figure(figsize=(15, 10))

for i, (p_var, m_var) in enumerate(variance_settings):

denoised_data = kalman_filter(time_series, process_variance=p_var, measurement_variance=m_var)

# 在不同的子图中绘制不同方差下的降噪效果

plt.subplot(2, 2, i+1)

plt.plot(data['Time'], time_series, label='Original Data', color='blue', alpha=0.6)

plt.plot(data['Time'], denoised_data, label=f'Denoised Data\n(p_var={p_var}, m_var={m_var})', color='red')

plt.xlabel('Time')

plt.ylabel('Price')

plt.title(f'Denoising with process_var={p_var}, measurement_var={m_var}')

plt.legend()

plt.tight_layout() # 自动调整子图布局

plt.show() # 显示图像

LogStatus(plt)

Sleep(1000 * 10)

原理说明:卡尔曼滤波通过递归计算来估计当前时刻的真实状态,并且能够动态调整对噪声的敏感度。卡尔曼滤波通过动态更新状态估计值和误差协方差,适应价格数据的动态变化,能实现对数据实时降噪。它适合实时数据,能跟踪数据变化。但是参数设置复杂,对噪声特性敏感。

参数解释:过程方差(process_variance)越小,卡尔曼滤波对变化的敏感度越低,滤波效果更强。测量方差(measurement_variance)控制对测量数据的信任程度。

图像解释:不同的方差组合下,卡尔曼滤波会产生不同程度的平滑效果。较小的过程方差使得数据更加平滑,而较大的过程方差则保留了更多的原始波动信息。

4. 结论

通过对比移动均线、傅立叶变换和卡尔曼滤波,我们可以发现: - 移动均线实现简单,但滞后性强; - 傅立叶变换能够有效去除高频噪声,但选择适当的频率阈值很重要; - 卡尔曼滤波能够自适应调整噪声的影响,效果较为灵活。

5. 数据获取的可靠性

有的同学可能会担心,使用这些降噪方法时是否会涉及未来数据。在优宽量化平台上,您完全可以放心,因为数据的获取是基于固定时间点逐步更新的,而不是一次性地进行更新。这种设计确保了策略在应用降噪处理时,仅依赖历史数据和实时更新的信息,而不会使用到未来数据,从而保持数据的真实性和策略的有效性。因此,您可以安心地在策略中运用这些降噪方法,以提高交易决策的准确性和稳健性。

6. 策略应用

文章最后放一个小彩蛋,使用降噪过后的数据进行双均线策略,对比原始的均线策略效果确实有所提升。大家可以以此为思路,开发更多应用。

'''backtest

start: 2024-09-01 00:00:00

end: 2024-09-30 23:59:59

period: 1h

basePeriod: 1m

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

args: [["ffthre",0.05]]

'''

import numpy as np

import pandas as pd

from scipy.fftpack import fft, ifft

ffthreshold = 0.05

slowPeriod = 60

fastPeriod = 20

def main():

def callBack_CTA(st):

data = pd.DataFrame(st["records"])

time_series = data['Close'].values

data['Time'] = range(len(data))

# 进行傅里叶变换

fft_values = fft(time_series)

frequencies = np.fft.fftfreq(len(time_series))

# 复制傅里叶变换值,进行降噪处理

filtered_fft_values = np.copy(fft_values)

# 根据阈值设置保留的频率范围,超过阈值的频率被设为 0

filtered_fft_values[np.abs(frequencies) > ffthreshold] = 0

# 进行逆傅里叶变换并提取实部(去掉复数部分)

filtered_time_series = ifft(filtered_fft_values)

filtered_time_series = np.real(filtered_time_series)

fftvalue = filtered_time_series.tolist()

emaSlow = TA.EMA(fftvalue, slowPeriod)

emaFast = TA.EMA(fftvalue, fastPeriod)

cross = ext.Cross(emaFast, emaSlow)

ext.PlotRecords(st["records"], "原始均线")

ext.PlotLine( "傅立叶变换",fftvalue[-1])

if st["position"]["amount"] <= 0 and cross > 2:

Log("金叉周期", cross, "当前持仓:", st["position"])

return 2 if st["position"]["amount"] < 0 else 1

elif st["position"]["amount"] >= 0 and cross < -2:

Log("死叉周期", cross, "当前持仓:", st["position"])

return -2 if st["position"]["amount"] > 0 else -1

ret = ext.CTA("sc2411", callBack_CTA)

注:策略需要点击交易和画图模版类库进行使用。

原始均线策略收益

降噪均线策略收益

- 奏响市场乐章:量化视角解析谐波形态

- 基于量化指标的蜡烛情绪动量趋势交易策略

- 期货行情引爆的导火线?量价关系的量化研究

- 商品期货“横久必跌”现象的量化实证研究

- 网红指标RSRS在商品期货中的应用

- 浅谈如何区分趋势和震荡行情:实战方法与代码详解

- 如何从学术论文中获取策略灵感:隔夜反转策略实现

- 量化揭秘纯碱2023年操盘手法:157倍的快乐你想象不到

- 智能数据驱动量化策略:基于聪明钱的日内交易模型

- 商品期货量化交易-TradingviewPine语言基础课程

- 国庆礼包:穿越牛熊市!网格交易策略揭秘与收益实战

- 深度解析商品期货中的胜率与盈亏比:交易策略成败的关键

- 商品期货风险控制:一个函数挽救400W的损失

- 优宽量化平台与CTP系统接口的深度融合及应用指南

- 商品期货「订单流」系列文章(四):微单和POC

- 探索优宽量化:状态栏按钮的全新应用(一)

- 商品期货「订单流」系列文章(三):供需失衡和堆积带

- 详解优宽量化交易平台API升级:提升策略设计体验

- 商品期货「订单流」系列文章(二):Delta指标

- 商品期货「订单流」系列文章(一):订单流概念介绍